Sign Up

School Account Sign Up

Lesson ID: 11579

Think credit is free money? Think again. Learn how borrowing really works and how to avoid turning quick purchases into long-term problems.

The Swipe That Isn’t Free

Picture this: you tap your card or phone, walk out with new shoes, and feel like you just won something. No cash left your hand. No problem… right?

Not exactly.

That “easy” purchase might follow you for months—or even years—if it turns into debt. Credit can be a powerful tool, but it can also quietly stack up into a serious financial problem if you don’t understand how it works.

Time to learn how to stay in control.

What Credit Really Means

Credit is borrowed money. When you use credit, you agree to pay it back later—usually with interest, which is the extra cost of borrowing.

Lenders (like banks or credit card companies) don’t lend money out of kindness. They make money from interest and fees. That’s their benefit. Your benefit is getting access to money when you need it—but there’s always a trade-off.

If you don’t pay back what you borrow on time, the cost grows.

Why People Use Credit

In today’s world, most people use credit at some point. It’s often used for:

Big purchases like cars, college, or homes

Emergencies when cash isn’t available

Building a credit history (which affects future loans, housing, and even jobs)

Used wisely, credit can help you move forward financially. Used carelessly, it can trap you in long-term debt.

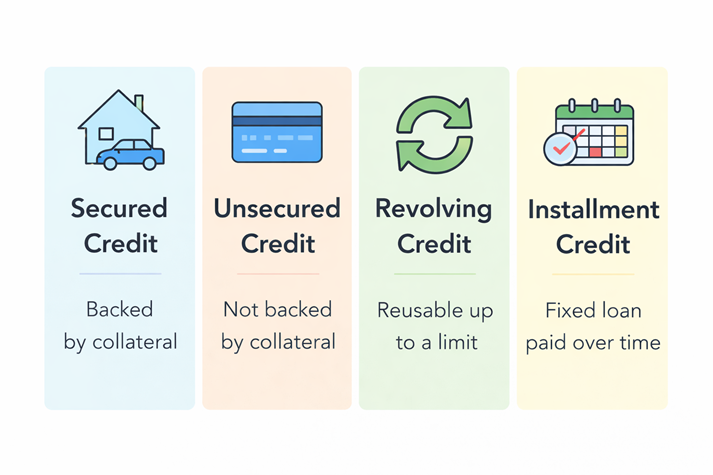

The Four Main Types of Credit

Understanding credit starts with knowing the different types. Each one works differently and comes with its own risks.

Secured Credit

This type of credit is backed by something valuable you own, called collateral. If payments aren’t made, the lender can take the item.

Examples:

Why people use it:

Risk:

Losing your property if you can’t pay

Unsecured Credit

This credit is not backed by collateral. Approval depends on your credit history and income.

Examples:

Why people use it:

Risk:

Revolving Credit

This allows you to borrow up to a limit, repay some or all of it, and borrow again.

Example:

How it works:

Why people use it:

Risk:

Installment Credit

This is a fixed loan paid back in equal payments over time.

Examples:

How it works:

Why people use it:

Risk:

The Real Risks of Borrowing

Borrowing money always comes with risk. Some of the most common include:

Interest piling up, making you pay far more than the original cost

Late fees and penalties

Damage to your credit score

Stress from ongoing debt

In serious cases, losing property or facing collections

At the same time, people still use credit because it solves immediate problems. That tension—short-term gain vs. long-term cost—is what makes credit tricky.

How to Stay in Control

Responsible borrowers follow a few key habits:

Only borrow what you can realistically repay.

Pay on time, every time.

Keep balances low.

Understand the terms before agreeing.

Have a plan before using credit—not after.

Think of credit like a tool. Used correctly, it builds your future. Used carelessly, it builds problems.

Where This Is Headed

Now that the basics of credit—and its risks—are clear, it’s time to put that knowledge into action.

In the Got It? section, you’ll break down real situations, identify smart choices, and practice handling credit like someone who knows exactly what they’re doing.

Supplies